The Union Budget for 2019 is essentially supplement to the interim budget presented before the General Elections 2019. Amidst global slowdown and volatile oil market, FM Nirmala Sitharaman chose to focus on consolidating the fiscal position, while ensuring new ease of living for the common masses. With the $5 trillion as the target, this budget looks to convert challenges into opportunities for the new and aspirational India

July 5, 2019 generated much buzz as Finance Minister Nirmala Sitharaman, being India’s first full-time woman Finance Minister, presented the first budget of the new Modi Government. Despite the strong mandate for a second term for Modi Government, the FM did not have the luxury of pacing her innings. So, she got off to a brisk start by taking the looming economic challenges head-on in her maiden budget.

A brief overview of changes brought out in the last five years were presented on the table, with the country geared to become a $3 trillion economy this year. An uptake to streamline education, encourage innovation, promote manufacturing and raise the ease of living and doing business across industries lie big on the cards. Technology stands at the fulcrum, as a series of measures undertaken to increase interoperability and accessibility across the value chain, automising tasks and reducing human error and intervention. These include facilitating electronic information-sharing across banks and companies that aid taxpayers with pre-filled tax returns, cutting out non-transparent human interfaces during the assessment process, forwarding the use of low-cost digital payment mechanisms by customers and merchants, alongside fostering a conducive intellectual environment that creates digital literacy. New-age themes, such as artificial intelligence, robotics, and IoT, are here to grow.

The impetus on technological advancement is closely linked to address large-scale infrastructural development, lying at the heart of the budgetary focus. Programmes such as Bharatmala, Dedicated Freight Corridors, Sagarmala and UDAN will continue to increase connectivity and competitiveness in the domestic market, with newer mediums such as rivers being utilised to decongest current routes. The government has also projected the necessity of public private partnerships across capital-intensive sectors such as railways that require over Rs 50 lakh crore from 2018 to 2030, in order to unleash faster development and get modernisation projects off the ground.

Welcome Budget: BMS

Bharatiya Mazdoor Sangh (BMS) welcomed the “Sasanmala” or chain of innovative governance mentioned in the Budget like Bharatmala, Jal Marg Vikas, UDAN schemes, ‘One nation-One grid’, GST, Mudra credit support, SHG women loan, encouraging EVs, Common mobility card, lowest external debt, fishing sector reforms, traditional industrial clusters, farmer supports and many others. In a statement BMS president Shri CK Saji Narayanan said it is also a welcome announcement in the budget that FDI policy will be consulted with stakeholders. “The Budget makes only a mention about labour codes. Already Government has assured that the spirit of synergy will be displayed while pushing forward the labour codes by consulting with Trade Unions and considering workers’ concerns. There are certain proposals mentioned in the Budget which needsto be discussed with Trade Unions as representing the major stakeholders affected before being implemented, Shri Saji Narayanan said.

Both rural and urban India received their own share of the limelight as the budget looked at creating conducive living conditions across localities. Schemes such as Pradhan Mantri Gram Sadak Yojana have received an investment target of Rs 80,250 crore to build 125,000 km of village roads. Meanwhile, electricity & LPG connections are to be extended to all willing rural families by 2022, while water facilities are to be brought about by 2024. Concurrently, a re-shift to zero-budget farming is proposed to double farmers’ incomes whilst a productivity boost in home development will keep the affordable housing goal up and running. Rapid urbanisation on the other side of the spectrum is seen as an opportunity than a challenge, with improvements in suburban and long-distance travel, attractive home and auto loans, start-up schemes and impartment of soft skills to set in a new ease of living.

Following are the major tax proposals by Union Finance Minister:

Income Tax

- There is no change in the rates of income tax for non-corporate Assessees and foreign companies.

- It is proposed to extend the benefit of reduced income tax rate of 25% for domestic companies having annual turnover of up to Rs 400 Crore (for the previous year 2017-18).

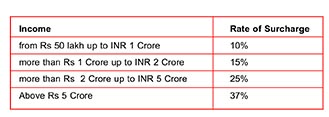

- There is no change in the rates of surcharge for corporate Assessees. In case of individual Assesses, the surcharge rates for FY 2019-20 are revised as shown in the table on next page.

- “Health and Education Cess” shall continue to be levied at the rate of 4% of income-tax including surcharge wherever applicable.

- It is proposed to provide interchangeability of PAN and Aadhaar to enable a person who does not have PAN but has Aadhaar to use Aadhaar in lieu of PAN. The Income Tax Department shall allot PAN to such person on the basis of Aadhaar after obtaining demographic data from the Unique Identification Authority of India.

- It is also proposed to provide that a person who has already linked his Aadhaar with his PAN may at his option use Aadhaar in place of PAN.

- To enable pensioners to have more disposable funds, the existing tax exemption of 40% of the total amount of payment from NPS Trust to the person at the time of closure or his opting out of the scheme, is proposed to be increased to 60%.

- To ensure that the Central Government employees get full deduction for contribution made by Central Government, it is proposed to increase the limit of section 80CCD deduction from existing 10% to 14% of contribution made by the Central Government to the account of its employee.

- Proposal to amend section 80C to enable the Central Government employees to have more options of tax saving investments under National Pension System by providing deduction for amount paid or deposited by them as a contribution to Tier-II account of pension scheme.

- It is also proposed to provide that a person whose income becomes lower than maximum amount not chargeable to tax due to claim of the rollover benefits of capital gains shall be required to furnish the return of income.

- It is proposed to insert a new section 80EEB to provide deduction in respect of interest on loan taken for purchase of an electric vehicle from any financial institution and NBFCs up to Rs 1.50 lakh.

- It is proposed to insert new section 80EEA to provide deduction of interest up to Rs 1.50 lakh on loan taken for residential house property having stamp duty value not exceeding Rs 45 lakh from any financial institution during 1st April, 2019 to 31st March 2020, provided that he does not own any residential house property on the date of sanction of loan.

- It is proposed to amend the definition of affordable housing to allow deduction to housing project, if a residential unit in the housing project have carpet area not exceeding 60 square meter in metropolitan cities or 90 square meter in cities or towns other than metropolitan and the stamp duty value does not exceed Rs 45 lakhs.

- Proposal to incentivize start-ups by allowing carried forward and set off of loss incurred in any year prior to the previous year against the income of the previous year on satisfaction of condition of fulfilment of at least 51% of the voting power being beneficially held by the same persons on the last day of the year or years in which the loss was incurred and setoff.

- Proposal to amend section 54GB, to incentivize investment in eligible start-ups, by extending the sun-set date of transfer of residential property for investment in eligible start-ups from 31st March 2019 to 31st March 2021 and relaxing the condition of minimum shareholding of 51% of share capital/ voting rights to 25%. Furthermore, the condition of restricting transfer of new asset being computer or computer software is also proposed to be relaxed from current 5 years to 3 years.

- Proposal for not considering deductor as an assessee in default in cases wherein failure to deduct TDS on payments made to a non-resident and such non-resident has filed its tax return, paid taxes on such income and has furnished a prescribed certificate from an accountant. It is also proposed to provide that in such cases, there would not be any corresponding disallowance of expenditure in the hands of deductor.

- It is proposed to provide exemption of interest income of a non-resident arising from borrowings by way of issue of rupee denominated bond referred to u/s 194LC, during the period from the 17th September, 2018 to 31st March, 2019.

- TDS to be deducted @2% on cash withdrawal by a person in excess of Rs 1 crore in a year from his bank account.

- TDS to be deducted @5% by Individual or HUF (who are not subjected to audit), on the payments made to a resident contractor or professional where such sum exceeds Rs 50 Lakhs in a year. However, such individuals or HUFs shall be able to deposit the TDS using their PAN and shall not be required to obtain TAN.

- TDS to be deducted @5% on the income component of life insurance pay-out on net basis instead of existing 1% on gross basis.

- To give impetus to the fund management activities in India, the conditions related to corpus of Rs 100 Crore and remuneration at arm’s length price have been proposed to be removed.

- Proposal to extend the anti-abuse provisions pertaining to buy back of shares to all the companies including listed companies w.e.f. 5th July 2019.

- Proposal to provide for cancellation of registration of the trust or institution for violation of the provision of any other law, which are material for the purposes of achieving its objects, where an order holding that such violation has occurred is either not contested or has become final. It is proposed to provide that at the time of registration it shall also be examined whether there has been any such violation by trust or institution seeking registration.

- Proposal to tax income arising from any sum of money paid, or any property situated in India transferred, on or after 5th July 2019 by a person resident in India to a person outside India shall be deemed to accrue or arise in India. However, in a DTAA situation, the relevant article of DTAA shall continue to apply for such gifts as well.

“The #BudgetForNewIndia has a roadmap to transform the agriculture sector of India. The Budget is one of hope and it is a budget that will boost India’s development in the 21st century” — Narendra Modi, Prime Minister

Goods and Services Tax

- Commissioner under GST to be given power, on the recommendation of GST Council to extend the due date for furnishing Annual Return, Reconciliation Statement (GSTR-9/9C).

- Enable Central Government to disburse refund amount of state taxes to the applicant.

- Prescribed class of registered person (to be specified by GST Council) shall be given an option to the recipient to make electronic payment.

- Formation of the National Appellate Authority for Advance Ruling for hearing appeals. Proposal provides for constitution of such authority, powers vested in such authority, procedure for filing appeals and rectification of orders issued by such authority.

- Threshold limit for levy of GST increased from Rs 20 lakhs to Rs 40 lakhs for the supplier of goods.

- It is proposed that Aadhaar authentication is mandatory for a specified class of new taxpayers and a certain class of existing registered taxpayers.

- Interest shall be charged on the net cash liability only except where the returns are filed subsequent to initiation of any proceedings under section 73 or 74 of the CGST Act.

- Any amount of electronic cash ledger can be transferred from one head to another head.

- An alternative composition scheme with maximum rate up to 3% is proposed for suppliers of services or mixed suppliers (not eligible under composition schemes) having annual turnover in preceding financial year up to Rs 50 Lakhs.

- Taxpayers registered under composition scheme or certain class of persons (having turnover less than Rs 5 crore) may furnish return annually along with quarterly payment of taxes instead of monthly returns.

- Empowering the National Anti-profiteering Authority to impose penalty equivalent to 10% of the profiteered amount if any registered person has profiteered.

“We shall further simplify procedures, incentivize performance, reduce red-tape and make the best use of technology just as we did earlier. I am confident we will achieve our goals” — Nirmala Sitharaman, Union Finance Minister

Customs

- Obtaining and utilizing any instrument by fraud, collusion, etc., would be a punishable offence and shall attract penalty not exceeding the face value of such instrument.

- Proper officer has been granted authority to screen/ scan with prior approval, a suspected person carrying secreted goods inside his body which is liable to confiscation and forward a report to nearest magistrate for further action.

- Countervailing duty may be imposed to such other article also where circumvention of same has been done by altering description, name, and composition of the article on which such duty has been imposed or by import of such article in an unassembled or disassembled form or by changing the country of its origin or export or in any other manner.

- Provision for Verification of Identity and Compliance provided to verify the identity of a person and other compliances undertaken by such person. In case of non-compliance, proper officer may suspend benefits arising out of import or export.

- Conditions have been specified under which the custody of seized goods will be given to certain specified persons.

- In case of search, seizure & arrest, proper officer to be empowered to provisionally attach bank account for a period not exceeding six months and release provisionally on fulfilment of specified conditions.

- For reducing litigations, cases covered under deemed closure proceedings under Section 28, no fine in lieu of confiscation shall be imposed.

- Enable the notified person to furnish departure manifest, in addition to the person in charge of conveyance.

Empowering proper officer to arrest a person who has committed offence outside India or on Indian Custom waters.

(The writer is a Chartered Accountant and heads the firm Akash Saraf & Associates)

Comments